Perspectives

On energy shocks and reality checks

By

On Friday, Feb. 4, 2022, U.S. West Texas Intermediate crude oil (WTI) rose above $92/B. Six months ago, that crude cost was about $62/B. The landed cost in Europe of U.S. LNG closed at $28.26 per million BTUs. One year ago, the comparable price was slightly over $6. Price escalations of 50% for crude oil and over 400% for natural gas have rightly been labeled an Energy Shock. Associated events have added to the pure economic anxiety. Watching OPEC + Russia’s failure to increase output in the face of rising prices brought back the uneasy feeling that unfriendly suppliers are back in charge of the oil market. Watching Russia manipulate gas supplies into Europe while it maneuvered to destabilize Ukraine was a reminder that energy can be deployed as a strategic weapon.

And then came the invasion.

These events have been a brutal reality check for consuming country governments. Only months ago, they were focused on how to fund and implement an energy transition. Now governments have to worry about keeping today’s lights on, combating non-transitory inflation and defending a world order where sovereign states don’t invade each other’s territory.

In the U.S., a Biden Administration that canceled the Keystone Pipeline and suspended leasing federal lands for oil/gas exploration is now asking the fracking industry to increase production. Simultaneously, it scours the globe for spare LNG to route into Europe. A Dutch government that took Shell to court over carbon emissions, driving the company to change its name and leave the country, now seeks Shell’s help to address the crisis. Meanwhile, one guesses that somewhere in Texas, industry old-timers are recalling that bumper sticker from the 1970s gas line that says: “Let the Bastards freeze in the Dark.”

Can we make something more constructive out of these unwelcome events?

The silver lining here is the greater clarity these events can bring to thinking about the Energy Transition. We are bumping into constraints that we can’t and shouldn’t ignore with the current shocks. There are major lessons here for policymakers and climate activists. A straightforward highway to a low emissions economy doesn’t exist. Getting from here to there will require a more complex and nuanced approach. Let’s explore this outlook.

One concern is how to prevent current issues from derailing steady progress towards lower emissions. In recent years some policymakers and climate activists have opposed any and all activities which continue the use of hydrocarbons. This activism achieved certain results. Efforts to suppress investment in fossil fuels progressed, with the Biden Administration’s policy efforts and Wall Street moves to limit funding oil and gas companies as noteworthy examples. The events mentioned above then arrived as unintended consequences. Clearly, some backing off of supply-side suppression is in order. The dilemma is how to allow this: 1) in a manner that would be positive for oil and gas supply without 2) conveying to the industry that it can go back to “business as usual.”

The first part is relatively straightforward. Consuming governments can reverse certain regulatory stances which have inhibited the industry from growing production. Greenlighting certain pipelines and reinitiating exploration leasing of federal lands are U.S. examples of such actions. A German decision to allow fracking would symbolize such a turn in Europe.

The second issue, sustaining Energy Transition progress, is the more challenging part. Here the issues involve accepting that more complicated path to Transition while ensuring that forward momentum is not lost. There are four adjustments that policymakers and the climate lobby can make which would help resolve this dilemma:

- Acknowledging that pursuing decarbonization solely with renewables + battery storage and Electric Vehicles (EVs) will not get the job done.

- Enabling lower-cost solutions that lower emissions today, even if they are not zero-carbon, would, for example, involve embracing natural gas as a critical bridge fuel.

- Supporting activities that pave the way for more extensive decarbonization projects during a Second Stage of Transition – two examples are the commercialization of new technologies and the buildout of needed infrastructure.

- Revamp fiscal policies and power market structures. Use approaches that support needed investments today while incentivizing steady progress towards lower emissions; these measures should convey that fossil fuel firms cannot revert to just focusing on their traditional business.

Pretending that renewables + battery storage and EVs can accomplish decarbonization seriously damages a realistic and pragmatic Transition implementation. Increasingly, the realization is setting in that electric grids become vulnerable with deep renewables penetration. Battery storage is a helpful but inadequate solution to their intermittency. The idea that the developing world can decarbonize solely via a transition to renewables is even more untenable – many of these nations’ grids are unstable in the base case. Further, these countries correctly anticipate needing copious amounts of new, firm generation to fuel their economic development.

Despite these stubborn facts, some political leaders and climate activists continue to offer only more renewables as the solution to every decarbonization challenge. The reasons for this mindset are important – it allows many to avoid considering whether the Transition will involve difficult tradeoffs; facing that reality would, in some cases, mean reversing opposition stances of long duration. Finally, many fear losing momentum on the narrative that fossil fuel use is the problem.

Attitudes of opposition to natural gas are perhaps the best illustration of these conflicted postures. Natural gas substitution for coal in power generation has been the biggest contributor to GHG emissions reduction in the U.S. It also has enabled a deeper penetration of intermittent renewables into power generation. Natural gas generation’s flexibility compensates for what renewables can’t provide in terms of load following and power quality. Still, many political leaders and environmental NGOs continue to oppose natural gas production and infrastructure – witness the successful killing of the Atlantic Coast pipeline and a new FERC leadership devoted to reinforcing regulatory barriers to new gas infrastructure. When combined with fervent advocacy of a climate emergency, such opposition suggests that it remains an article of faith that renewables + storage is an adequate solution. This faith misleads the public on all-in costs and grid resiliency, blocks ready progress on other fronts, and thus is becoming a serious obstacle to climate progress. Admitting that such is the case would be Step One on the path to a Feasible Transition.

This brings us to the second adjustment, rethinking attitudes towards a broad suite of steps that are beneficial now, even if they are not by nature fully zero carbon. Today’s posture of opposition is justified as needed to wean economies off hydrocarbon use. Done precipitously or without economically viable substitutes, however, this approach produces those uninvited consequences – power failures, elevated energy prices and geopolitical risks. Popular reaction to such outcomes then stokes opposition to climate policies. Such opposition has resulted in political and policy reversals and the loss of precious time regretfully. Current events suggest that these risks are becoming even more acute.

There is an alternative to a “renewables-only” solution that carries the seeds of its reversal within it. It is to integrate renewables with proven, lower carbon solutions as a stage – a first stage in the Feasible Transition. LNG and nuclear energy provide excellent examples of this staging approach. Maximizing today’s global natural gas production and feeding many such supplies into LNG holds great potential for immediately reducing coal-fired power generation in the developing world. China today starts up three new coal plants per month. India, South Africa and numerous other developing countries continue to build coal-fired plants. With billions spent on renewables, even Germany still burns domestic lignite and imported coal. Now that Russia’s actions have underscored a need for reliable, secure energy, Germany is reconsidering its nuclear plant closures and plans to build the LNG import facilities it now regrets not having constructed years ago.

Ramping up gas production and feeding LNG into these economies will reduce GHG emissions versus current trends. It will also mute price and geopolitical pressures. Such sequencing is a core component of the Feasible Transition. Do what helps now and then enable today’s good solutions to improve within some reasonable time horizon.

This brings up the third element of the Feasible Transition – enabling needed new technologies to be commercialized and associated infrastructure to get built. There needs to be more understanding of how energy technologies are commercialized. Initial demonstration plants should not be targeted for ‘kill’ when their economics or operations fall short of initial promises. Such results are more the rule than the exception. Next-generation technologies need to be allowed to demonstrate their potential over several projects during which problems are corrected, and economics improved. Moving from all-out opposition to any impacts on the environment towards enabling necessary infrastructure to be built will also pave the way for a successful Stage Two Transition.

Some examples serve to illustrate the point. Gas-fired power plants can be retrofitted with carbon capture equipment. Such technology exists today, and many firms are at work on improvements. Other forms of power generation, like the Allam Cycle, provide built-in carbon capture. The bottleneck here is the economical disposal of the captured CO2. Disposal should be relatively easy in Texas and Louisiana, where depleted oil reservoirs provide secure storage and producing fields offer enhanced oil recovery opportunities. CO2 projects in these locations can be enabled by realistic environmental rules governing what constitutes secure geologic storage of the captured gas.

Elsewhere CO2 disposal is a formidable barrier. The construction of CO2 pipelines can overcome this barrier. Some such pipelines already exist; their technology is mature, and their operation is well understood. Standing in the way is the same all-out environmental opposition which killed the Atlantic Coast pipeline. Moving forward, can we see our way to supporting the pipeline infrastructure that will enable the decarbonization of power generation?

A growing realization that other forms of infrastructure will be needed enhances the case for doing so. Long-distance power transmission lines are such an example. These would enable Oklahoma wind power and Arizona solar to reach markets not blessed by such efficient renewable resources. Such lines also will involve some, usually modest, environmental impacts. In recent years, local NIMBY opposition to unsightly power lines has successfully blocked their construction. Here we must now ask, what issues should get priority? If climate is the emergency many say it is, does that not support the case for building new long-distance transmission, even at the cost of some local impacts?

Next-generation nuclear reactors are another example of technologies that we can choose to enable or obstruct. Many of these technologies have been under development for years, even decades. Several are approaching deployment. The next-gen reactors assert that their technologies can improve and even resolve issues that have bedeviled nuclear power in recent decades. Their small modular designs might offer relief from sticker shock prices that have led to new projects being deemed a “bet the company” proposition. Alternative coolants, such as molten salts or liquid sodium, imply that plant shutdowns can be accomplished without the backup facilities and human interventions that failed at Three Mile Island and Fukushima. How can we tell if these promising technologies are real and deserving of support?

We can only find out through the process of technology commercialization. The companies involved, including NuScale and Bill Gates’ TerraPower, will have to test their technologies by building demonstration facilities. Should these prove their technology’s feasibility at scale, they will be ready to work with utilities on commercial plants. The environmental community can play an enabling role here by asking the right questions. Do the technologies mostly deliver on their promised safety improvements? Can firms fix the issues, and there likely will be some, discovered by building and operating the demonstration plant? Do the technologies offer on balance improved safety versus existing large Light Water Reactors? If the answer to these questions is yes, other questions follow. Are we prepared to enable their deployment via reasonable licensing and regulatory reviews? If yes, what modifications should be adopted on matters ranging from site footprints to nuclear waste disposal?

The environmental communities’ answers to these questions will demonstrate the coherence of their approach to climate. Again it is essential to pause and understand the environmental community’s reluctance to relax its unflinching opposition stance. Stopping things that impact the environment is built into its DNA. Moreover, it knows how deeply fossil fuels are embedded into the economy. It knows too that nuclear comes with demonstrated historical risks. There is a lot to digest here if the NGOs are to accept the tradeoffs involved in enabling non-renewable projects and technologies to move forward. This must be added to their concern that dropping a stance of active opposition would allow fossil fuel firms and nuclear utilities to revert to business as usual.

The staging concept advocated in this blog is sensitive to these risks. This brings us to the fourth item, revised power market structures and fiscal policies. Changes here can help alleviate some climate lobby concerns. The Feasible Transition will require U.S. merchant power markets to be restructured. At present, these markets do a woeful job of generating the capital needed for funding the generation and transmission assets needed for Transition; as events in Texas and California demonstrated, they also fail at incentivizing resiliency. Continuing to force more intermittent power into merchant markets will worsen that problem. These markets need capacity pricing structures that work, i.e., which generate capital and incentivize utilities to invest in both resiliency and decarbonization. In a few locations today, deals are being struck which marry proper market incentives with utility commitments to decarbonize. Illinois’ restructuring to keep three nuclear plants from closing and recent North Carolina legislation are examples of such constructive approaches.

Addressing today’s incoherent fiscal policies offers an opportunity to avoid that reversion to the business as usual issue. Today’s fiscal policies are a mess. They amount to mandates and subsidies for renewables and EVs, regulatory suppression of nuclear and fossil fuel development, and hardly anything in terms of a price on carbon; this mix suppresses energy supply and subsidizes winners who collectively cannot provide a solution while doing next to nothing to address energy demand. The unsurprising result – energy price inflation and stalling progress on emissions.

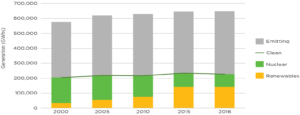

Another look at Germany shows how this policy mix has failed to achieve its goals. Germany has showered subsidies on renewables, prohibited new nuclear and fracking of its gas reserves, and moved aggressively to shut its existing nuclear sites. Here’s how that’s playing out:

2018 German Electricity Net Generation Mix (GWh)

Source: Scott Madden Consultancy

In terms of decarbonization, this is appropriately labeled “spinning our wheels.” The better alternative would keep existing nuclear operating, bring back recently shut plants and foster continued gas for coal substitution. Combine this supply-side work with a fiscal policy that communicates to the industry that there is no alternative to Transition. The fiscal policy to do this is a firm, gradually increasing price on carbon. This approach will free firms to approve long-life supply projects today with the knowledge that these will have to be de-carbonized or replaced in a second stage. It thus also incentivizes the technology and infrastructure deployments needed for that Feasible Transition Stage Two. Fossil fuel and utility firms who take a business as usual approach will risk becoming increasingly uncompetitive.

The Environmental Community has done a noteworthy service. It has put the climate issue front and center in our politics, financial markets and the board room. However, this was accomplished via advocacy that emphasized potential dangers while brushing aside dissenting views and collateral issues. This approach is now reaching diminishing returns. It is time to get more serious about accomplishing the tasks that leaders and climate activists have insisted must happen most urgently. That requires a return to the world of “better though not perfect,” improving the good over time, and not pretending that the Transition that can be achieved will be easy, cheap or wholly green.